Expectations And Analysis Of Current And Forward Data.

Analysis of microeconomic data, macroeconomic data, political data, geo-political data, and monetary policy with commentary on it.

United States:

The United States remains on a deflationary path given the monetary policy measures and the continuing improvements in global supply chains that have allowed and are allowing supply and demand to stabilize, although government legislative measures are complicating the soft-landing path as they're generating supply-side inflationary pressures. As mentioned before, the inflation forecast remains to the downside in the short run and to the upside in the long run due to forward energy price reflation due to government legislative policy measures that generate supply-side inflation. Given the fact that those inflationary pressures are supply-driven, monetary policy can't help lower those inflationary pressures as monetary policy has only tools to reduce demand-side inflationary pressures, which raised concerns over a plausible overreaction to the forward energy price reflation as it could cause a Volcker-like event that nobody really wants.

Overall, the United States remains strong given the continuing improvements in the job market given by government legislative measures and the improvements in price stability given by monetary policy measures. The decrease in geopolitical tensions has been notable, but they remain high despite attempts by top United States officials to lower them. Thursday's Gross Domestic Product data release and Friday's Core PCE data release are expected to continue in the same trend, showing a strong United States with complicated inflationary pressures that monetary policy can't lower. Fiscal and legislative policies should be guided towards decreasing supply-side inflationary pressures. Wednesday's interest rate decision is to remain the same; forward expectations over monetary policy remain the same, with precautionary positioning towards approaching the more than plausible energy price inflation shock due to previously explained reasons. Something to point out is that the previous Core PCE inflation data have been nearly the same when it comes to supply and demand-driven inflationary pressures, with demand-driven inflation upticking in core PCE inflation since June 2022; but remaining contained in the 2% range.

Markets are echoing the previously mentioned expectations over the dollar's performance; although markets remain focused on betting on the best-case scenario, which is the achievement of the soft-landing as employment data remains strong and price stability is slowly but steadily approaching the 2% target, markets seem to not realize yet the forward energy price reflation, which will more than probably have a black swan effect in markets into year-end and early into next year. As mentioned before, positioning remains prudent given the inflationary risks in the current scenario.

The current supply-driven price action in grain commodities, given warfare, will be reflected in the inflation readings in the coming months. Extreme climate conditions are also limiting the supply of these commodities to the market, although production is expected to be high, at least in the United States. Therefore, these supply-driven inflationary pressures are expected to ease earlier next year, unlike the previously explained energy supply-driven inflationary pressures. How to hedge it will be explained ( part of it has already been explained before ) after this week's previously mentioned key Gross Domestic Product data release, Core PCE data release, and interest rate decision. Jerome Powell's remarks are expected to be in line with previously given statements as employment data remains strong, allowing monetary policy to be focused on price stability.

Europe:

The Euro Area core inflation rate continues to trend on the expected path, although it remains persistent, and consumers expectations over inflation remain contained. As mentioned before, European countries measures over electric grid stability have not only made recession fears vanish but also lowered forward energy price inflation expectations in the Euro Area as supply exceeds demand, unlike the United States, which is under energy supply-side inflation. Although European countries measures over production have increased forward supply-side inflation risks, which is causing some European countries leaders to lose support from their citizens, they should enhance legislative and fiscal policy measures towards lowering supply-side inflationary pressures that monetary policy can't lower, as monetary policy has only tools to lower demand-side inflationary pressures. European government measures towards ensuring key goods security prove how attentive European countries leaders are, but they should, as mentioned before, enhance fiscal and legislative policies towards decreasing supply-side inflationary pressures.

The European Central Bank is expected to maintain the hawkish but nimble stance that Ms. Lagarde has been stating since the monetary policy tightening path started; thus, Ms. Lagarde's press conference after this week's interest rate decision is expected to be in line with previously given statements. Markets have already priced in a 6% peak rate; therefore, this week's interest rate decision is expected to deliver a hike as demand-side inflationary pressures persist and continue to hike until after inflation reaches the 2% inflation target.

United Kingdom:

The United Kingdom's inflationary pressures are easing, although its inflation remains behind its major G7 peers. Lower inflation has lifted sentiment but still remains far above the 2% target; thus, monetary policy is expected to remain restrictive until after inflation reaches the target. Markets previously priced in a peak rate that almost reached 7%, the current SONIA curve signals that markets have priced in a peak rate above the post-inflation data consensus; thus, there is a gap for risk-on price action in United Kingdom markets given the spread between the previous and current peak rate consensus.

Although positioning remains risk-off, this is due to recent volatile price action in the British Pound that makes United Kingdom markets volatile. A thing to point out is that United Kingdom's government granted bonds valuations are on discount relative to government measures and forward inflation; the only factor that makes United Kingdom markets have downside is the supply-side inflation risks adhered to by still persistent supply chain issues related to Brexit. Recent United Kingdom government initiatives have lowered those worries, but they still remain.

Asia:

China:

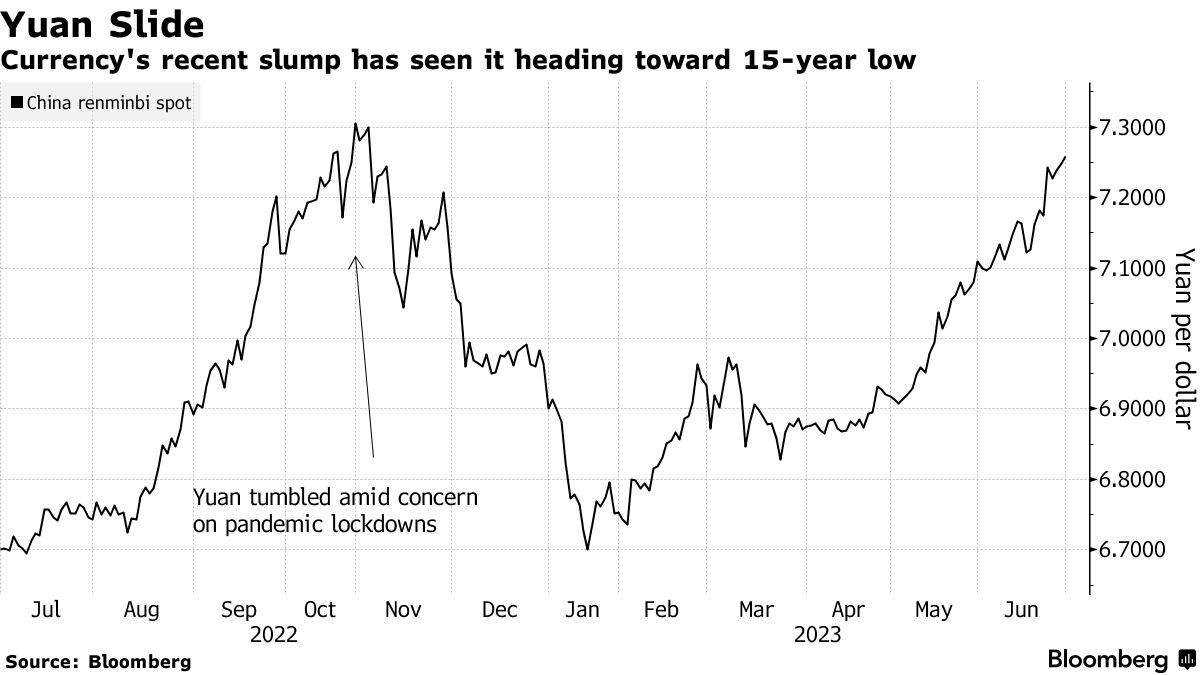

China's economy continues to grow; there are still worries over China's economy given worrisome youth employment data, although China's employment remains stable. Government fiscal policy measures and monetary policy measures are ensuring that China's economy doesn't contract into recession. China's increase in electricity consumption indicates that industrial activity is growing, which will likely be reflected in forward manufacturing production and industrial production statistics. This is good news as it signals a forward increase in global trade flows and domestic flows that enhance the Chinese Yuan valuation, which is currently being supported by the People's Bank of China given recent price action.

{kind=link}

As mentioned before, geopolitical tensions remain high even though there have been intentions by allies of the United States towards lowering tensions, including top United States officials trying to lower tensions with a climate envoy. China remains focused on ensuring that the One China principle is being respected, which it isn't, as Western countries top officials state that they respect the One China principle but do the contrary. Thus, forward expectations remain the same.

Japan:

Japanese inflation seems to have peaked, but price pressures are expected to increase as there are supply-driven grain commodity price pressures into year-end. And supply-driven energy commodity price pressures into year-end and early into next year, and forward in time if governments don't address the supply-side inflationary pressures through fiscal and legislative policies, as monetary policy can't address supply-side inflationary pressures. Bank of Japan's inflation projections are coherent and in line with current and forward expectations over the current scenario, markets are still betting on a shift in monetary policy given previous remarks from the Bank of Japan's governor Ueda. Expectations for the Japanese economy remain the same.

Do feel free to share, leave a comment, and subscribe to Quantuan Research Substack if you want, by using the next buttons.

It's not about the money (the research is free); it's about sending a message (delivering alpha to the reader).